Reverse Logistics Market Growth: Product Returns, Circular Economy & Forecast to 2034

How increasing product returns, recycling strategies, and circular supply chain models are reshaping operational efficiency in the reverse logistics industry

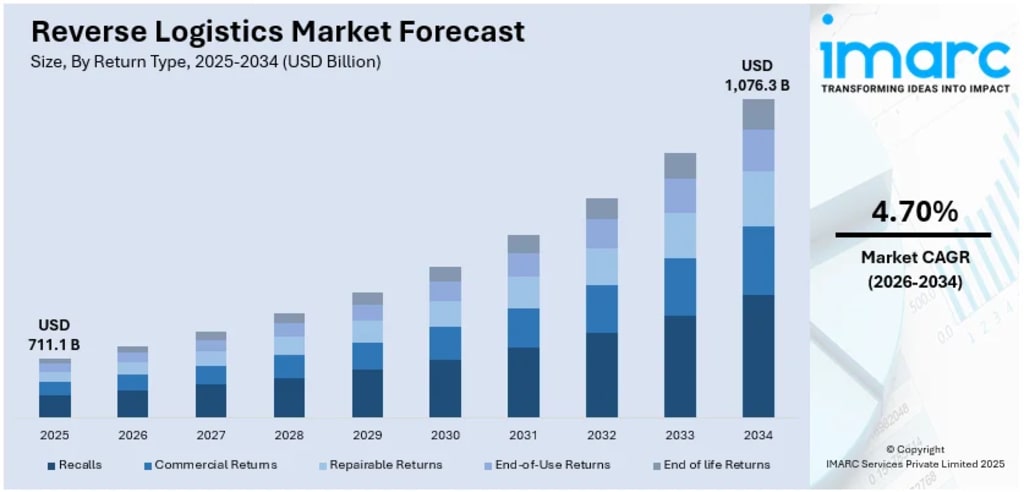

The global reverse logistics market size reached USD 711.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 1,076.3 Billion by 2034, exhibiting a growth rate (CAGR) of 4.70% during 2026-2034. Environmental concerns and regulations, the rise of e-commerce and online returns, the emphasis on sustainability, technological advancements, such as blockchain and the Internet of Things (IoT), the adoption of circular economy principles, and increasing consumer expectations for hassle-free returns are some of the factors supporting the market growth.

The Scale of the Return Economy

The numbers behind the reverse logistics industry are striking. The global market is projected to reach USD 1,076.3 Billion, reflecting a fundamental structural shift in how supply chains are designed and operated. This is no longer a niche concern for warehouse managers; it is a boardroom-level strategic issue.

At its core, reverse logistics covers the full lifecycle of a product after it leaves the buyer's hands, including transportation, warehousing, reselling, refurbishment, refund management, and end-of-life disposal. According to IMARC Group's comprehensive reverse logistics market analysis, North America leads the global landscape, backed by advanced logistics infrastructure, high e-commerce penetration, and stringent regulatory frameworks that mandate responsible waste management.

Forces Shaping the Reverse Logistics Market

E-Commerce Returns as the Primary Growth Engine

The explosion of online shopping has fundamentally changed return behavior. Studies suggest that online return rates can run two to three times higher than those from physical retail, partly because consumers cannot inspect items before buying. Impulse purchases, sizing mismatches, and quality dissatisfaction drive a constant flow of goods back through supply chains.

Major e-commerce platforms are responding by investing in dedicated return infrastructure. Companies like Happy Returns have built nationwide drop-off networks that consolidate returns before bulk shipping them back to retailers, cutting per-item return costs significantly. UPS and FedEx have both expanded reverse logistics service lines to capture this growing segment.

Environmental Regulations Tightening the Compliance Landscape

Governments worldwide are making proper product disposal a legal obligation, not just a best practice. The European Union's Waste Electrical and Electronic Equipment (WEEE) Directive compels manufacturers to fund and organize the collection and recycling of electronic goods. In the United States, Extended Producer Responsibility (EPR) legislation is gaining momentum at the state level, with California, Oregon, and Colorado having passed packaging-focused EPR laws that ripple upstream into reverse logistics planning.

India's E-Waste Management Rules similarly require producers and importers to meet collection and channelization targets, adding compliance pressure that is accelerating reverse logistics investment in the Asia-Pacific region.

Sustainability and the Circular Economy Imperative

Corporate ESG commitments are making reverse logistics a tool for differentiation. Brands that can credibly demonstrate product take-back programs, refurbishment pipelines, and waste diversion metrics are gaining preference among environmentally conscious consumers. Industry data shows that sustainable purchasing decisions now influence over a third of purchase choices in key markets.

Apple's trade-in program recycles millions of devices annually, recovering rare earth elements and reducing demand for virgin materials. Caterpillar's remanufacturing division restores used heavy equipment components to original specifications, selling them at a fraction of new part prices while dramatically cutting material waste.

Segmentation Deep Dive

By Return Type: Commercial Returns Lead the Way

Among all return categories, commercial returns hold the largest share of the Reverse Logistics Market. This segment is driven by the complexity of modern product portfolios, where customization, compatibility requirements, and high return rates from e-commerce create a constant need for specialized reverse processing. Recalls, repairable returns, end-of-use returns, and end-of-life returns complete the landscape, each demanding distinct handling protocols.

By Service:

Transportation and Warehousing at the Core

Transportation and warehousing together form the operational backbone of reverse logistics. Innovations in route consolidation are lowering the carbon cost and financial cost of reverse shipping. Smart warehousing technologies, including automated sorting systems and robotics, are being rapidly deployed to handle the high volume and variability of returned goods with greater speed and accuracy.

Reselling is emerging as a high-margin opportunity. Consumers increasingly trust refurbished and certified second-hand goods, supported by quality assurance programs from brands and third-party resellers alike. The secondhand electronics market alone is valued in the tens of billions globally and is growing faster than new device sales in several categories.

By End User:

E-Commerce, Automotive, and Consumer Electronics Drive Volume

E-commerce remains the dominant end user, but the automotive and consumer electronics sectors are growing rapidly. The automotive aftermarket generates significant repairable return flows for parts, and electronics manufacturers face constant pressure to manage product take-backs under regulatory mandates. Pharmaceuticals and luxury goods represent specialized verticals with strict chain-of-custody requirements in the returns process.

Technology as the Competitive Differentiator in the Reverse Logistics Market

The industry is undergoing rapid transformation and scale-up through several technological fronts:

Artificial Intelligence and Machine Learning are enabling predictive return management, helping retailers anticipate return volumes by region, product category, and season, which reduces excess inventory accumulation.

Blockchain is being piloted for end-to-end transparency in return supply chains, allowing brands to verify the authenticity and condition history of returned goods before reselling or refurbishing.

IoT-enabled tracking gives logistics providers real-time visibility into returned shipments, reducing processing times and improving disposition accuracy.

Robotic Process Automation (RPA) is streamlining refund management authorization workflows, reducing manual effort and processing times.

Recent News and Developments

March 2026: UPS announced an expansion of its Returns Manager platform, integrating AI-driven disposition logic that automatically routes returned goods to the highest-value outcome, whether resale, refurbishment, or recycling, reducing landfill diversion costs for retail clients.

November 2025: DB Schenker partnered with a European electronics manufacturer to launch a dedicated circular economy returns hub in the Netherlands, designed to process over 2 million units annually, supporting EU WEEE compliance targets.

August 2025: FedEx expanded its consolidation returns network in Southeast Asia, targeting the region's rapidly growing e-commerce segment, with a stated goal of reducing per-unit reverse shipping costs for platform sellers by up to 30%.

April 2024: The U.S. Environmental Protection Agency (EPA) released updated guidance encouraging companies to integrate reverse logistics planning into their Sustainability Performance Plans, reinforcing the policy link between waste reduction and supply chain design.

Policy and Regulatory Tailwinds

Beyond the EU and U.S., regulatory momentum is building across multiple geographies:

China's Green Supply Chain Initiative encourages large manufacturers and retailers to implement take-back and recycling programs as part of national environmental targets.

India's Plastic Waste Management Rules require producers to manage the end-of-life return of plastic packaging, creating new reverse logistics obligations across the FMCG and e-commerce sectors.

Canada's Zero Plastic Waste Agenda is pushing brands toward packaging take-back schemes that inherently require reverse logistics infrastructure.

These policy frameworks are not just compliance burdens; they are creating structured demand for reverse logistics services, effectively guaranteeing a growing client base for providers who invest in compliant solutions now.

Strategic Outlook: Where the Market Is Headed

The Reverse Logistics Market is at an inflection point. What began as a cost center is being repositioned as a value recovery engine, a sustainability credential, and a customer loyalty tool simultaneously. Companies that view returns as a problem to minimize are being outpaced by those who view them as an asset to optimize.

The sector continues to attract significant investment from private equity, venture capital, and corporate strategic funds. Startups specializing in AI-powered return disposition, sustainable packaging take-back, and blockchain-verified refurbishment are attracting multi-million-dollar funding rounds, signaling long-term confidence in the market's trajectory.

For stakeholders seeking granular segmentation data, regional breakdowns, competitive benchmarking, and strategic forecasting, exploring the full IMARC Group Reverse Logistics Market Report offers a rigorous foundation for informed decision-making in this rapidly evolving space.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Vinyl Record Market Outlook: Retro Trends, Independent Artists & Forecast to 2034

In a world saturated with instant, algorithm-driven music consumption, the vinyl record has staged one of the most unexpected commercial revivals in modern consumer history. Turntables are selling out. Pressing plants have backlogs stretching months. Independent record stores are not just surviving but expanding. The numbers tell a story that would have seemed improbable just two decades ago.

By Suhaira Yusufabout 13 hours ago in Futurism

The Fears of AI And How Much Fun It Can Be

ChatGPT has come a long way, as has AI in general. There are those people who are scared of it, and for understandable reasons. People fear that as technologies advance, they’ll be replaced in the workforce. Then, there are the fears that AI could evolve into something that brings us to the brink of extinction.

By Jason Morton8 days ago in Futurism

Sea Salt Market Significant Growth at 3.7%

Overview The global sea salt market is poised for steady growth over the next decade, driven by rising demand across food, wellness, and industrial applications. The Global Sea Salt Market is expected to be worth around USD 28.0 billion by 2034, up from USD 19.5 billion in 2024, and is projected to grow at a CAGR of 3.7% from 2025 to 2034. Increasing consumer preference for natural, mineral-rich salts and expanding use in gourmet and specialty products are expected to support this consistent market expansion worldwide.

By Hayden Kulas5 days ago in Futurism

I Live By the Bottle

For about a week I had the Norovirus. The Norovirus is a gastrointestinal virus that causes vomiting and diarrhea. Most people get over it within three days. It is troublesome for the elderly and young children, as well as people with medical conditions. I, myself, have a rare medical condition called Nephrogenic Diabetes Insipidus.

By Sid Aaron Hirjiabout 18 hours ago in Education

Comments

There are no comments for this story

Be the first to respond and start the conversation.