Why the Urinary Tract Infection Treatment Market Is Quietly Becoming a Major Healthcare Story

As infections rise across age groups and antibiotic resistance reshapes treatment decisions, the global UTI treatment market is entering a new phase of demand, innovation, and long-term healthcare relevance.

Urinary tract infections rarely dominate healthcare headlines, yet they remain one of the most common and disruptive bacterial infections affecting people worldwide. They are often dismissed as routine or “easy to treat,” but that perception is changing. Today, urinary tract infections, or UTIs, are no longer just a short-term inconvenience handled with a quick prescription. They are becoming a growing global healthcare challenge tied to aging populations, recurrent infections, hospital-acquired complications, antibiotic resistance, and the urgent need for more targeted treatment options.

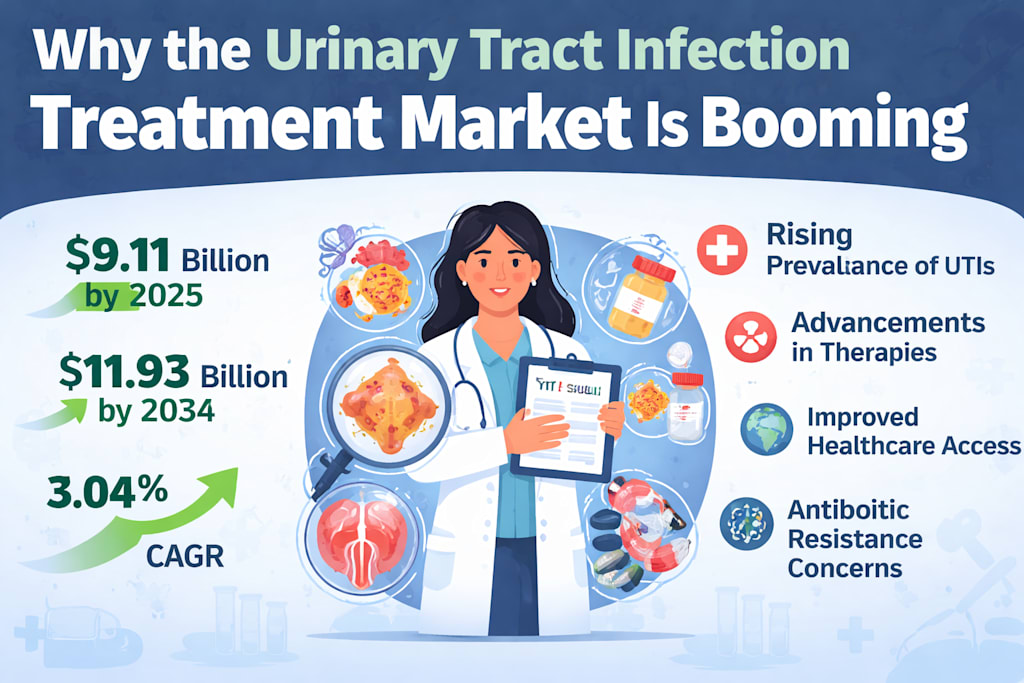

That is precisely why the Urinary Tract Infection Treatment Market is gaining attention. According to Renub Research, the global Urinary Tract Infection Treatment Industry is expected to reach US$ 9.11 billion in 2025 and grow further to US$ 11.93 billion by 2034, expanding at a CAGR of 3.04% from 2026 to 2034. That steady rise reflects more than just pharmaceutical sales. It signals a deeper shift in how healthcare systems, clinicians, and patients are approaching diagnosis, treatment, and prevention in a category that affects millions every year.

At its core, UTI treatment includes therapies designed to address infections that occur anywhere in the urinary tract, including the bladder, urethra, ureters, and kidneys. Most cases are caused by bacteria, especially Escherichia coli, and many are treated with antibiotics. However, the treatment landscape is widening. Alongside conventional drug therapy, healthcare providers are increasingly exploring symptom relief medications, probiotics, cranberry-based preventive options, self-testing tools, and non-antibiotic therapies for recurrent infections. That broader treatment ecosystem is one of the reasons the market is expanding beyond its traditional pharmaceutical boundaries.

One of the strongest forces driving this market is the rising prevalence of UTIs across nearly every demographic group. Women remain the largest affected segment, but they are far from the only one. Children, older adults, people with diabetes, catheter users, and individuals with weakened immune systems are all contributing to rising case volumes. As healthcare systems improve screening and patients become more aware of symptoms, more infections are being diagnosed earlier and treated more consistently. The market is also benefiting from the high recurrence rate of UTIs, especially among women, which often leads to repeated treatment cycles, follow-up visits, and long-term management strategies rather than one-time prescriptions.

This pattern is not minor in scale. UTIs are among the most widespread bacterial infections globally, and their burden is significant enough to influence public health systems, outpatient care models, pharmacy sales, and hospital infection control programs. In practical terms, this means demand is not limited to one geography or one patient type. It is broad, recurring, and deeply connected to everyday healthcare delivery.

Another major reason the market is evolving is the rapid change in treatment expectations. For years, antibiotics were the default and almost exclusive answer. Today, that approach is being challenged. Doctors and researchers are under increasing pressure to balance effective infection control with the growing threat of antimicrobial resistance. That has pushed the industry toward more thoughtful prescribing, more precise diagnostics, and more innovation in both antibiotic and non-antibiotic treatment pathways.

This shift matters because not all UTIs behave the same way. Some are uncomplicated and respond quickly to standard therapy. Others are persistent, recurrent, or linked to more complex medical conditions such as kidney disorders, structural abnormalities, or diabetes. These cases often require more intensive management, broader-spectrum antibiotics, intravenous therapies, or longer treatment durations. As a result, the market is no longer defined by just “simple infection treatment.” It now includes a layered treatment model ranging from home care and pharmacy access to advanced hospital-based interventions.

The innovation pipeline is also becoming more interesting than many people realize. Pharmaceutical and healthcare companies are not only working on better antibiotics but also investing in supportive tools that make diagnosis and early action easier. Home testing and self-screening are gaining momentum, especially in consumer-focused healthcare markets. This reflects a broader trend in medicine: people want faster answers, easier access, and more control over common health conditions. When applied to UTI treatment, that creates a strong commercial opportunity. A patient who can identify symptoms early and access treatment faster is not only more likely to recover sooner, but also more likely to engage with diagnostic products, telemedicine services, and pharmacy-based care pathways.

At the same time, the market faces a serious structural challenge: antimicrobial resistance. This is not just a scientific issue; it is a commercial and public health problem. The overuse and misuse of antibiotics have allowed resistant bacterial strains to become more common, making some infections harder and more expensive to treat. That creates pressure on the industry to develop newer therapies while also making clinicians more cautious in prescribing. In the long run, this challenge may actually accelerate innovation, but in the short term it complicates treatment decisions and raises the cost of care.

Patient behavior adds another layer of complexity. Recurrence and poor compliance remain major barriers in UTI treatment. Some patients stop medication too early, delay care, or fail to address lifestyle factors that contribute to repeated infections. This is particularly important in recurrent UTI cases, where the market increasingly overlaps with preventive care, chronic condition management, and patient education. In other words, the future of this market is not just about curing infection. It is also about reducing repeat episodes and improving treatment adherence.

From a product perspective, several treatment classes continue to shape the market. Quinolones remain important due to their broad-spectrum activity and deep tissue penetration, especially in cases where first-line therapies are not suitable. However, safety concerns and resistance trends are limiting their use in some settings. Cephalosporins, on the other hand, continue to hold strong relevance because of their broad bacterial coverage and comparatively favorable safety profile, particularly for pediatric, elderly, and pregnant patient populations. These differences show how the market is becoming more segmented and clinically nuanced rather than one-size-fits-all.

The complicated UTI treatment segment is especially important because it reflects the intersection of infection treatment with broader chronic disease and hospital care trends. Patients with diabetes, catheter use, renal complications, or anatomical abnormalities often require more intensive treatment plans. This creates higher-value demand for hospital care, specialist consultation, injectable therapies, and close monitoring. In market terms, complicated UTI cases are especially significant because they generate more resource-intensive care and stronger demand across multiple healthcare service channels.

Hospitals also play a critical role in this market, particularly because many severe or catheter-associated infections emerge in institutional care settings. Hospital-acquired UTIs remain a major burden, and this continues to drive demand for rapid diagnostics, infection-control protocols, and hospital-grade therapies. That gives the hospital treatment segment long-term strategic importance, especially as healthcare systems worldwide focus more heavily on quality metrics, infection prevention, and antibiotic stewardship.

Geographically, the market presents a compelling mix of maturity and expansion. The United States remains one of the most established UTI treatment markets, supported by strong healthcare infrastructure, widespread diagnostics, and active pharmaceutical innovation. The country also benefits from urgent care networks, retail clinics, and telemedicine channels that make treatment more accessible and immediate. These delivery models are helping redefine how common infections are treated in everyday healthcare.

The United Kingdom represents a different but equally important model. Its evidence-based public healthcare framework supports standardized treatment pathways and a more disciplined approach to antibiotic use. That makes the UK a notable example of how stewardship and treatment demand can coexist within a cost-conscious health system.

Meanwhile, India stands out as one of the most important high-growth markets. With a large population, improving healthcare access, expanding diagnostic infrastructure, and widespread availability of low-cost generic medications, India is well positioned for sustained market expansion. Rising awareness, private healthcare growth, and government-backed health improvements are all supporting stronger demand. At the same time, India also reflects one of the market’s biggest tensions: how to expand treatment access without worsening antibiotic misuse. That balance will be central to the country’s long-term role in this sector.

The broader global picture suggests that UTI treatment is increasingly tied to preventive care, women’s health, elderly care, antimicrobial policy, and healthcare accessibility. This is what makes the market more important than it may first appear. It is not just a narrow infection category. It is part of a larger healthcare story involving public health behavior, outpatient convenience, pharmaceutical innovation, and chronic disease management.

For companies operating in this space, the opportunity is no longer limited to selling standard antibiotics. Growth will likely come from a combination of better-targeted therapies, resistance-conscious prescribing solutions, self-testing tools, preventive products, and smarter treatment pathways. The companies that understand this broader shift will be better positioned than those still relying on older, volume-driven treatment models.

For patients and healthcare systems, the message is equally clear: UTIs may be common, but they are not trivial. As recurrence rises and resistance spreads, the need for smarter, earlier, and more personalized treatment is becoming urgent. That urgency is exactly what is fueling the next stage of this market.

Final Thoughts

The Urinary Tract Infection Treatment Market may not always attract flashy attention, but it is becoming one of the more meaningful healthcare segments to watch. A growing patient base, rising awareness, evolving therapies, and increasing concern around antibiotic resistance are all reshaping the industry. With Renub Research projecting the market to grow from US$ 9.11 billion in 2025 to US$ 11.93 billion by 2034, the sector is clearly moving from routine treatment territory into a more strategic, innovation-driven healthcare category.

About the Creator

The Dollar in Crisis

How Global Conflicts Are Reshaping Its Power The US dollar has long stood as the dominant global currency, a symbol of economic stability and geopolitical power. For decades, nations have relied on the dollar for international trade, central bank reserves, and financial transactions. However, in the context of ongoing global conflicts and geopolitical tensions, the dollar is facing new pressures that threaten its supremacy. The current war-driven landscape is reshaping global finance, trade networks, and the perception of the dollar as the world’s safe haven.

By Wings of Time 8 days ago in Trader

Australia Horticulture Market 2026: Fresh Produce Demand, Smart Farming & Export Growth

Australia Horticulture Market Overview The Australia horticulture market is a vital segment of the country’s agriculture sector, encompassing the cultivation of fruits, vegetables, nuts, flowers and ornamental plants. The industry plays a key role in ensuring food security, supporting exports and driving rural economic development.

By Amyra Singh8 days ago in Trader

The Portrait of Matteo

Seventeen-year-old Manny got off a public bus at a busy intersection in downtown Philadelphia. When the bus released its brakes and passed his narrow view, he checked whether the art museum across the street was still there. He had been visiting it every day that week but wondered for a second the veracity of its presence. Now, the spring sun betrayed its gray highlights, giving it a warm glow.

By Paul Aaron Domenick6 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.